Advisor Perspective

Advisor Perspective

JMG’s Investment Process, Designed Around You (Part 3 – Investment Selection and Implementation)

By Bill German, Chief Investment Officer, Principal, CFP® and John White, Principal, CFA, CFP®

This article is the third in a four-part series. In the previous articles we discussed the first two steps in the overall investment process: Client Analysis and Portfolio Design. In this edition, we will discuss the third step in our process, Investment Selection and Implementation, in which your advisor, with guidance from JMG’s Investment Committee, chooses the specific investments you will hold in your portfolio.

Our next and final article will cover Ongoing Management, the process your advisor uses to respond to changing economic and market conditions to optimize your after-tax results over time.

Investment Selection

Once your advisor has developed your Portfolio Design, the next task is selecting the specific investments which are used to implement the portfolio. The JMG Investment Committee maintains a list of securities across the asset classes which are approved for advisors to use in portfolios. The Investment Research Team provides analysis for evaluating investments prior to approval and conducts ongoing due diligence to ensure that each investment continues to support our investment rationale and its role in our overall portfolio. Our approach varies based on the asset classes we are investing in and our clients’ needs.

Passive Equity Funds

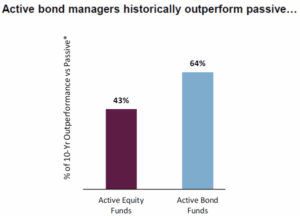

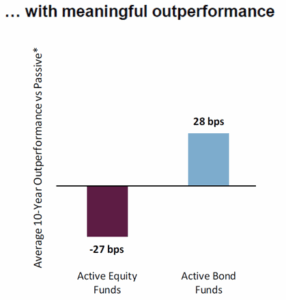

For equity investments, or stocks, we believe that markets are highly efficient. According to Morningstar, most active equity managers underperform their indexes over time.i While some managers will beat the market some of the time, rarely has a manager demonstrated the ability to beat the market consistently, regardless of market conditions, and the ability to select the next top performing manager has been similarly ephemeral. Therefore, instead of trying to select the next winner, we typically invest in broadly diversified low-cost strategies, typically in exchange-traded funds, due to their better tax efficiency. Even amongst these funds there are choices to be made. We review the expenses, the trading spreads, and trading volumes, for example, to ensure that we will be able to enter and exit a position without moving the market.

Active Fixed Income Funds

For fixed income investments, in contrast to equities, there is some evidence that active managers can add value over passive investments.ii Over time, fixed income managers have demonstrated the ability to outperform their indexes more consistently over a wider range of market conditions.

- In part, this is a result of how the fixed income market is structured. Whereas in the equity indexes, the largest, most successful companies are the largest holdings, in fixed income indexes the largest holdings are often the largest debtors, and the largest debtor does not make the best investment.

- In addition, several factors favor firms with scale in trading, operations, and research to outperform, including:

-

- Bonds and other fixed income instruments are not traded over an exchange, but rather through direct transactions between institutional trading desks.

- There are substantially more bonds in the marketplace than there are stocks.

As a result, for fixed income investments we typically use well-established active managers who have a record of outperforming their indexes net of fees and expenses. A typical analysis includes screening funds based on size, performance, and cost, followed by deeper analysis of the manager and specific strategy focused on “the 6 Ps.”

- People – Who are the people specifically supporting this strategy and how does the team benefit from the overall firm capabilities? Does the experience and track record of the team indicate an ability to implement consistently over time?

- Philosophy – How does the manager view the markets? What inefficiencies have they identified which they believe will give them an edge?

- Process – How do they select securities? And how do they know when to sell them? Do they implement their approach consistently?

- Portfolio – Does their portfolio reflect their philosophy and process or are there inconsistencies?

- Performance – How has the portfolio performed? Are periods of under or out performance consistent with their overall approach?

- Price – Do they offer low-cost, institutional share classes which are competitively priced?

Separately Managed Accounts

While we typically use broadly diversified mutual funds and ETFs for most of our clients, there are circumstances where holding individual securities makes sense, including stocks, bonds and options. In these cases, which typically involve seeking a specific type of outcome beyond benchmark relative performance, we partner with third-party managers who specialize in meeting the specific needs of our clients. Reasons for investing with specialized managers include, but are not limited to:

- A client who is looking for consistency of income and stable returns from owning bonds directly.

- A client whose tax situation would benefit from accumulating tax-losses in a portion of their portfolio, while maintaining consistent overall returns.

- A client who has a concentrated stock position and would like to manage risk around it, or tax efficiently transition out of the position over time.

Private or Alternative Investments

Finally, for investors who qualify, we employ private investments to enhance our client portfolios. Private investments are called private because they are bought and sold in private transactions, away from the public markets. They are also sometimes referred to as “alternative investments.” This contrasts with the “traditional investments” of public equity, bonds, and cash. To qualify for these investments an investor must meet certain requirements based on income or investable assets, and these requirements vary by strategy. Due to the limited liquidity of these investments, we typically limit their allocation to a relatively small portion of a client’s portfolio.

We categorize our private investments based on the role we intend for them to play in client portfolios. Some investments are intended to enhance returns, while others provide more risk mitigation. For example:

- Return enhancing alternatives: Private Equity, Private Debt, Private Real Estate

- Risk reducing or diversifying: Hedge Funds

That said, an important characteristic of alternative investments is that there is a wide dispersion of risk and return among managers, even within specific categories of investment. It is therefore essential that we do the research and due diligence to understand the specific characteristics of the manager’s investment style as it is expressed in a specific fund, and to understand the role it can play in a client portfolio. As with fixed income funds above, we used the 6 P framework. The difference is that even more emphasis is put on the specific strategy, with an emphasis on understanding the risk and return expectations so we know how it will fit into a portfolio.

Over time, we have built strong relationships with managers who provide access to strategies with long histories of attractive performance which provide us with confidence in their ability to help our clients meet their goals. Some of the underlying strategies our managers use have limited capacity and are closed to new, direct investment.

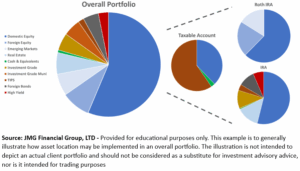

Implementation – Asset Location – Ensuring your Portfolio is Tax Efficient

Investing your portfolio does not end with investment selection. We also consider your tax situation. There are two main elements to this: asset location, and your transition plan.

Asset location involves deciding how to map your portfolio to your specific accounts. This can have significant impact on your after-tax return because every security has a specific tax profile as do the different accounts. We want to align these as best we can in order to minimize the tax drag on your portfolio.

As an example, a high yield bond fund producing 7% pre-tax returns in a taxable account of a client in the 33% marginal tax bracket would only produce a 4.76% return after taxes. If the same bond were invested in a tax deferred IRA, the account would retain the full 7%, reinvesting it each year. Compounding at the higher 7% rate produces a significantly higher long-term return than having to pay taxes each year, even after accounting for the taxes paid when the funds are withdrawn from the IRA.

The result is that we invest different types of accounts very differently. We typically invest Roth accounts aggressively, typically 100% in equities, even for conservative clients, since the Roth accounts have the longest time horizon and are completely tax free. In contrast, taxable accounts have competing goals of liquidity, growth, and tax efficiency. As a result, we blend taxable accounts with lower risk investments, such as tax exempt bonds, with more aggressive equity funds which pay qualified dividends. Finally, traditional tax-deferred IRA accounts are an ideal location for tax-inefficient investments like high yield bonds or alternative investments.

Transition planning considers the tax consequences of moving from one portfolio to another. This primarily relates to unrealized capital gains held in taxable accounts. Here we consider your planning objectives, your long-term plan, as well as your target portfolio. For example, for clients who have charitable objectives, we may set highly appreciated stocks aside for charitable purposes. Clients who are not projected to sell a security during their lifetime may benefit from holding it until they can pass it on to their heirs with a step up in tax basis. On the other hand, a client who is projected to need liquidity may be better served by selling an asset sooner. Of course, where possible, we will place trades to adjust your portfolio where the tax costs are lowest – in your retirement accounts. In addition, we use losses to offset gains when available.

Summary

As your financial advisor builds your portfolio, he or she relies on the work that the JMG Research Team and Investment Committee has done to build an approved list of high quality, consistent investment options, and to educate the financial advisors about these investments. Based on this work, your advisor can confidently select the funds or strategies that align with your Portfolio Design to support your goals and objectives. Once the investments have been selected and the portfolio has been invested, the advisor determines the most tax efficient way to deploy your portfolio, and the best approach to transition to this portfolio.

In our next article, we will describe how your advisor monitors your portfolios, adapting to market conditions over time. Ongoing Management is step four of our process.

If you have any questions about this process, please reach out to your financial advisor.

Sources:

i Morningstar US Active/Passive Barometer, Midyear 2025

ii Ahead of the Curve – PIMCO Advisor Playbook – Q1 2025

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).