Thoughts on the First Quarter

INVESTMENT COMMITTEE COMMENTARY March 2022

Inflation, interest rates, oil prices and the war in Ukraine continued to impact the investment markets in March. While progress in the U.S. with COVID-19 continues, the pandemic is not fully behind us as companies figure out how and when to bring employees back to their offices. The most recent March employment surveys reported strong numbers, consistent with the expansion phase of the economic cycle. The U.S. unemployment rate for March stands at 3.6%. Growth in the labor force continued, but the growth was uneven. The civilian labor force for men is back on the pre-pandemic trend line. However, the labor force for women remains approximately 850,000 workers short.

The Federal Reserve (Fed) has dual policy goals: maximum sustainable employment and stable prices. In March, it became clear the Fed will focus more on inflation as employment data continues to strengthen. On March 16th, the Fed approved its first interest rate hike in three years and signaled six additional hikes in 2022. The combination of higher inflation and a tightening Fed policy led to an increase in interest rates and the worst performing quarter for bonds since 1980. In March, the yield on 10-year U.S. Treasuries rose from 1.84% to 2.32%, up from 1.52% at the beginning of the year. It is more likely headline inflation will peak in mid-2022 and then fall by year end, but likely towards a 4%-5% level, above the Fed’s target inflation rate of 2%.

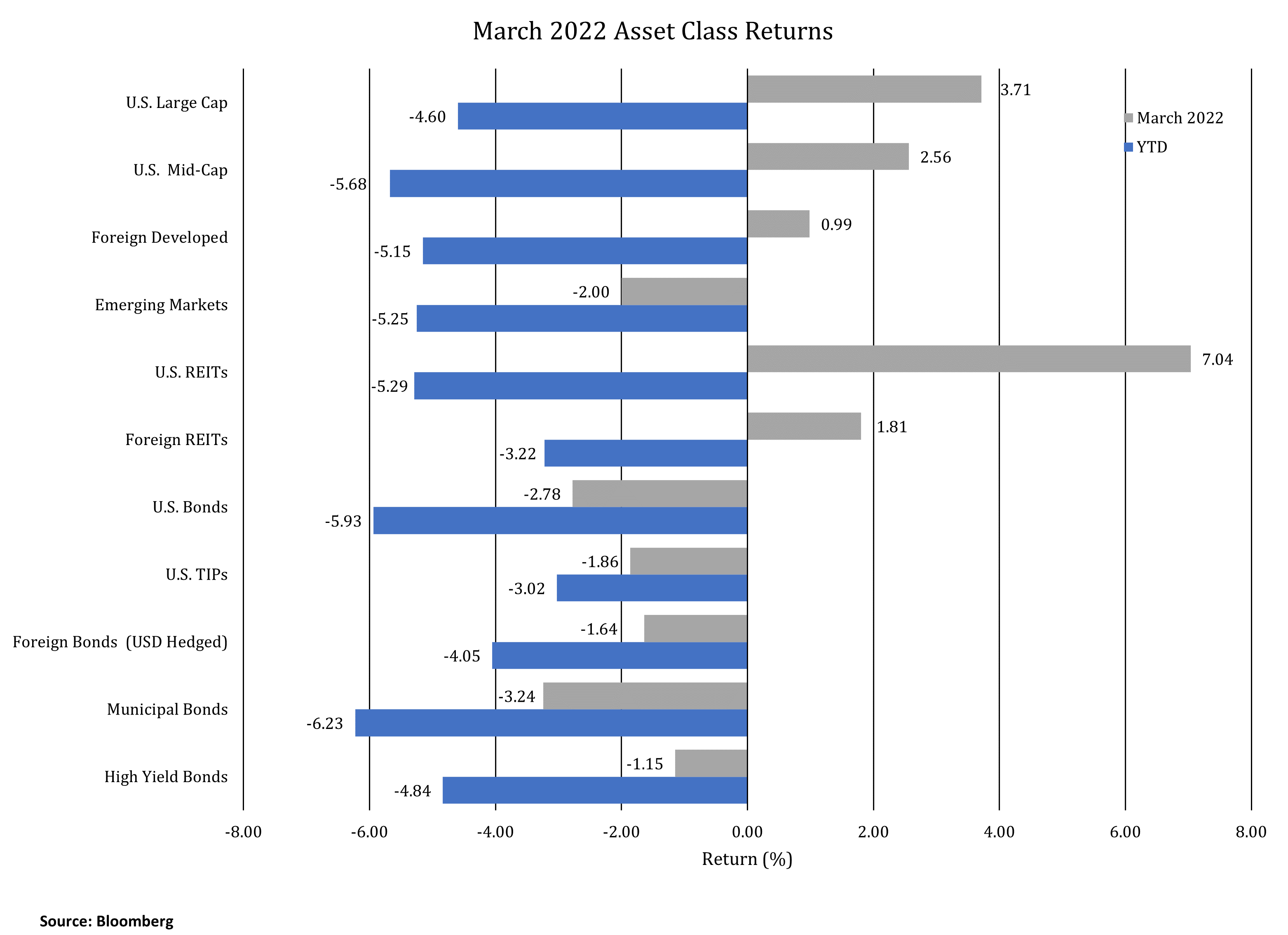

Equities had positive performance in March, recovering a portion of the declines experienced in January and February. The S&P 500 gained 3.7% and U.S. REITs were up 7.0%. Still, the equity market indexes are down approximately 5% for the year. Emerging markets (EM) declined 2.0% in March. COVID outbreaks in China contributed to EM underperformance. Supply chain disruptions could continue as Chinese government lockdowns are closing factories and restricting residents in important trade centers such as Shanghai.

Thoughts on the First Quarter

It is rare for there to be similar negative performance across both equity and fixed income asset classes. However, in the first quarter, several factors led to this outcome. In January, the Omicron variant paused the economic recovery. In addition, lingering supply chain issues, U.S. energy policy and the war in Ukraine sent commodity prices surging. From a beginning of the year price of $75 per barrel, crude oil closed as high as $124 per barrel in March, before finishing the quarter at $100.

Inflation is now more widespread, as reflected in a spike in the prices of intermediate producer goods. Transportation costs have risen 19% from a year ago resulting in increased prices as most everything we make and buy spends time in a truck. Food prices both at home and away from home are up. With labor force shortages, nominal wage growth is now at 6.7% for production and nonsupervisory workers. As a result, the inflation rate has moved to its highest level in 40 years. The Fed will use its limited tools to try to hold back inflation without overcompensating and pushing the economy into recession. In March, the U.S. Treasury curve inverted which some view as a leading indicator of recession. While recession risks are higher, we see recession as still a lower risk in 2022. Recession in Europe due to the Ukrainian war has a higher probability.

Ultimately, Fed policy will play an important role as to how economic issues are resolved. It now seems clear the Fed will have difficulty getting inflation back to 2% target levels any time soon. Managing through this period will be a delicate process.

The Good News

With a confluence of difficult issues, we see some positives. The U.S. economy and investment markets have been resilient. In the U.S., the economy is again restarting from COVID shutdowns. People are coming back into the labor force and finding jobs. Corporate earnings are holding up and consensus S&P 500 earnings estimates look strong into 2024. Equity market valuations have fallen to more reasonable levels. Some equity asset classes had positive returns in March, reversing a two month market correction. Interest rates rising to more normal levels, while negative for bond values in the short term, is positive for returns going forward. Over time, investors will benefit from bonds paying higher yields and we believe bonds will continue to provide diversification and a ballast against equity volatility and risks.

Final Comments

- We do not recommend investment market timing tied to geopolitical events or news cycles. We have maintained strategic allocations and opportunistically rebalanced portfolios with the associated increased volatility.

- Diversification is working. For example, allocations to TIPS and hedged foreign bonds are adding value relative to U.S. intermediate duration investment grade bonds. Equity asset classes are taking turns with relative performance. In such uncertain times as now, it is more important than ever to stay diversified.

Please contact your JMG advisor with questions or concerns.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this writing, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG Financial Group, Ltd. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm nor a certified public accounting firm and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure statement discussing advisory services and fees is available for review upon request.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment. Market Segment (index representation) as follows: U.S. Large Cap (S&P 500 Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S. Bonds (Bloomberg US Aggregate Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bonds (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).