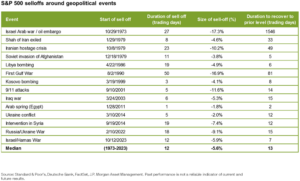

Keeping the Iran War in Context

INVESTMENT COMMITTEE COMMENTARY February 2026

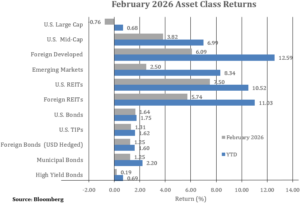

The U.S. stock market ended the month on a disappointing note, with the S&P 500 closing February in negative territory. After a strong start in January, the technology rally cooled, as investors grew concerned about market concentration. Tech stocks tumbled, while defensive and cyclical stocks trended higher. Mega-cap stocks, which carried the equity markets throughout 2025, have seen increased volatility in 2026. Some investors, questioning big-tech valuations, are seizing an opportunity to take profits. In February, money moved to more traditional value sectors, such as energy, materials, and consumer staples.

In contrast to the S&P 500, U.S. mid cap stocks, small cap stocks, and real estate investment trusts (REITs) had strong performance. Also, foreign developed and emerging markets stocks performed well in February but are being challenged with new developments from the conflicts in Iran and the Middle East.

The S&P 500 fell 0.8% in February but remains marginally higher for the year through February. Foreign developed and emerging market equities also rose 6.1% and 2.5%, respectively, and are continuing strong returns to start 2026.

Bonds had positive performance in February as 10-year Treasury yields fell from 4.26% to 3.97%. The Bloomberg U.S. Aggregate Bond Index (AGG) gained 1.6% for the month. Other bond sub-indexes also had positive performance although high yield bonds had a modestly lower return of 0.2% with emerging issues in private credit and direct corporate lending.

Keeping the Iran War in Context

Regarding the situation in the Middle East and Iran, the situation remains fluid. In the near term, the market reaction is higher market volatility, higher oil and energy prices and lower stock prices on rising geopolitical risks. However, markets have historically been resilient during wars and crises. Short-term market reactions to geopolitical shocks are often negative, but brief. One-year returns after geopolitical shocks are often positive. Geopolitical shocks and wars create short-term uncertainty but have not historically altered the long-term growth trajectory of U.S. equities. Staying invested and maintaining a long-term perspective has been a consistent theme in successful market outcomes.

The long term impacts of this are likely to depend on the effect that the war has on energy supplies. While the U.S. has become a net exporter of oil, most other major economies depend on oil and natural gas imported from the Persian Gulf. The war has already forced energy producers to take production offline due to limited storage capacity and to protect infrastructure. As a result, energy prices have risen sharply. Rising energy prices are negative for stocks because businesses depend on energy and higher energy prices tend to depress overall economic activity. But commodity markets adapt over time as new supplies come online, and consumers adjust demand. As a result, the effect of an energy shock is mitigated over time.

Looking past the near-term volatility resulting from the war with Iran, it’s important to keep in mind the key trends which have been impacting the markets, including AI sentiment, economic growth and central bank policy.

- AI Sentiment. The markets have recently shown concern over the ability of software companies to protect their businesses in the face of AI competition. This has manifested itself in sharply lower valuations for companies such as Salesforce, Adobe, Intuit, and others. It has also resulted in private credit investors seeking to pull capital from private funds which are large lenders to software companies. The level of redemption requests has led to funds implementing gates to slow redemptions or taking other measures to protect shareholders. Importantly, while JMG recommends private investments, JMG has broadly avoided direct recommendations to private credit investments and loans to Software as a Service companies. The fixed income and private loan managers we recommend have the ability to navigate away from credit risks and to also invest opportunistically, as warranted. In our opinion, AI presents both an opportunity and a threat to companies of all types, and that there will be winners and losers. Companies who can adapt will be able to improve margins and possibly market share, while the laggards will struggle. We purposefully own broadly diversified portfolios so that our clients can benefit from this process of “creative destruction.”

- Economic Growth. For the past year, new job creation has been lackluster, and the recent jobs reports have reinforced that trend. However, the U.S. economy has continued to grow, and productivity has continued to improve. Stimulus in areas outside the U.S. has resulted in rising stock markets in Europe, Japan, and emerging markets. The growth of the U.S. economy has been largely driven by investment in AI infrastructure. As AI providers achieve scale and continue to improve their models, the rest of the economy is adapting, finding ways to utilize AI to make their businesses more efficient and effective. An ongoing conflict in the Middle East could be a headwind to global growth over the near to intermediate term. Whether this would be enough to offset the current drivers of growth is yet to be seen.

- Central Bank Policy. Faced with slowing job creation and potential inflation from tariffs and a possible energy crisis, the Fed is expected to take a cautious approach, yet stands ready to shift policy based on market conditions. With relatively healthy current interest rates, the Fed has some flexibility to respond to changes in the economy, and we expect them to continue to implement a data driven policy.

We continue to diligently monitor the investment environment and the opportunities and risks that may impact recommended allocations.

If you have any questions, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

This content is provided for educational purposes only. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice.

A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).