Economic Reversals – Hints of a Cooling Economy

INVESTMENT COMMITTEE COMMENTARY November 2022

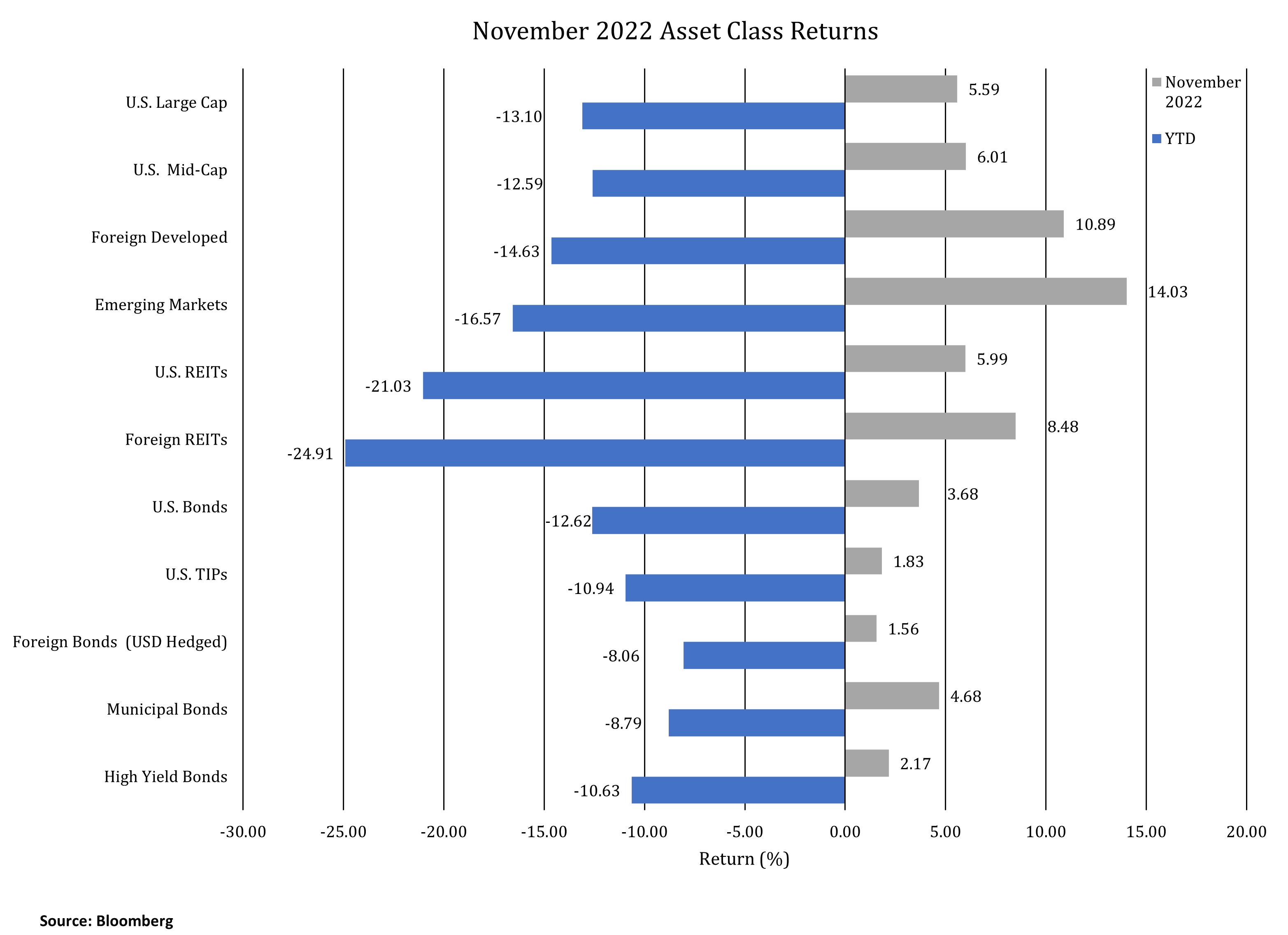

Following comments by Federal Reserve (Fed) Chairman Jerome Powell, stocks and bonds rallied in November. The S&P 500 rose for the second straight month, up 5.6%. Foreign developed equities and emerging markets also rebounded with strong gains of 10.9% and 14.0%, respectively. Emerging markets had their best monthly performance since March 2016 as global money managers, including Morgan Stanley, predicted a peak in the U.S. dollar. U.S. real estate investment trusts (REITs) gained 6.0%.

For the month, the yield on 10-year Treasuries fell from 4.08% to 3.70%. As a result, intermediate investment grade bonds gained 3.7%. Most fixed income categories rose over 1.5% in November. Notably, municipal bonds were up 4.8%.

Currently, the key performance catalyst for stocks and bonds is Fed monetary policy. Powell announced on November 30th that the pace of interest rate hikes can slow as soon as December. This likely means the Fed will raise interest rates by 50 basis points (0.5%) in December, ending a string of 75 basis point hikes. The Fed must balance concerns about inflation with those of slowing economic growth and falling earnings as we move into 2023. The rate of employment and industrial production have both remained strong despite the Fed’s tightening so far, but there are signs of weakness.

Economic Reversals – Hints of a Cooling Economy

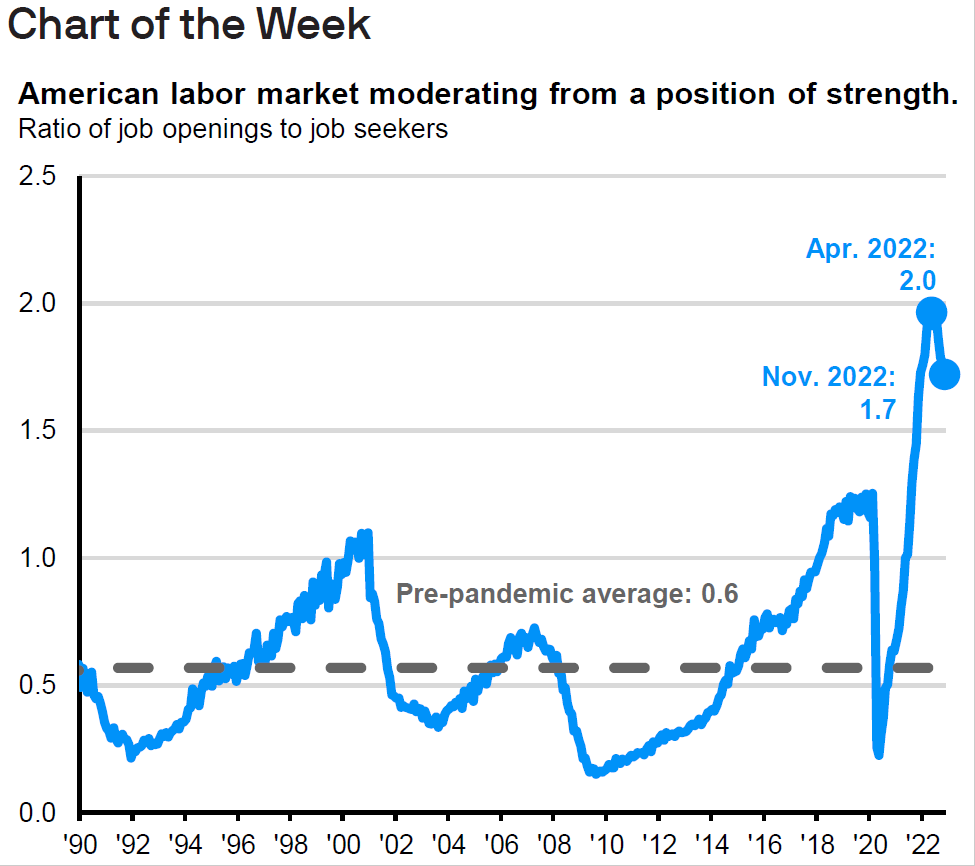

The most recent employment reports, while presenting stronger headline numbers, mixed results. The Job Openings and Labor Turnover Survey (JOLTS) presents data on job openings, hires and separations. As illustrated in the chart below, there continues to be more job openings than job seekers which is positive. The trend through the COVID pandemic is displayed and while the ratio recently turned down, job openings remain at a higher level, consistent with late-stage economic expansion.

Source: Bureau of Labor Statistics, J.P. Morgan Asset Management

However, underlying data in the Employment Household Survey was not robust. The labor force has declined for the last three months (and five of the last six months). Also, the number of persons employed has fallen for the last two months. The unemployment rate remains at 3.7% and has been that level through most of 2022. The bottom line from available employment data is that the economy is making forward progress but at a diminishing pace as Fed tightening appears to be impacting job creation.

It has been interesting to see how the labor market has been inversely impacting the investment markets. Negative employment statistic releases help investors gain conviction that inflation is cooling. Positive employment numbers have been catalysts to equity market declines. In both cases the markets are anticipating how the Fed will react regarding interest rate policy.

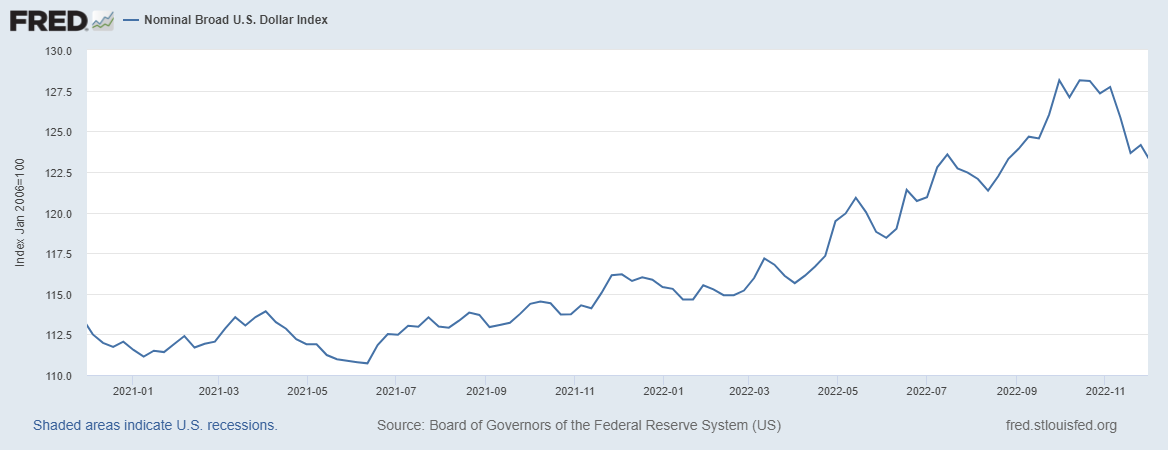

The strength of the U.S. dollar has also recently reversed direction. The following chart from the Fed shows the U.S. dollar index (DVY) has generally risen for the last two years. However, it has recently weakened as investors see some moderation in inflation. The weaker dollar contributed to stronger foreign and emerging markets performance in November. After a two-year long rally, some believe the dollar has peaked, especially with the recent sharp reversal.

Source: Federal Reserve

In summary, U.S. economic conditions appear to be weakening and while not there yet, an economic cycle peak and recession may be closer. However, the combination of lower stock valuations and higher interest rates mean that portfolio assets are positioned for higher growth for long-term investors.

If you have any questions, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment. Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).