2022 In Review/2023 Views

INVESTMENT COMMITTEE COMMENTARY December 2022

The positive momentum of October and November for stocks and bonds faded in December. Global central banks signaled that they were still committed to aggressively hiking rates. Economic data showed clear signs of slowing growth, and several negative earnings announcements raised concerns of an earnings recession in 2023.

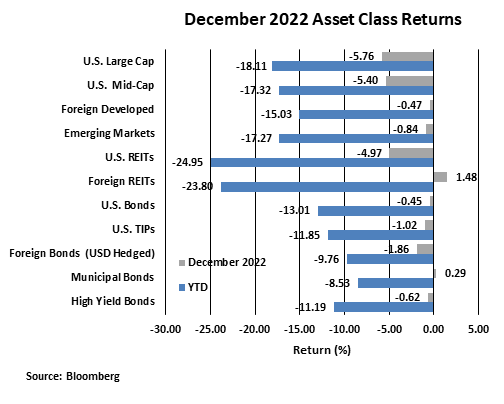

In December, the Fed first revealed that they expected to take the fed funds rate above 5% (from the current 4.375%), which was higher than market expectations. Then, economic data released in mid-December, including regional manufacturing indices and the November retail sales report, showed economic activity was slowing. Also, both the European Central Bank and the Bank of Japan surprised markets with hawkish policy decisions, providing yet another reminder to investors that rates will continue to rise in 2023 despite clearly slowing global economic growth. Stocks dropped from mid-December on, and the S&P 500 ended the month of December with a loss of 5.8%.

Internationally, foreign markets outperformed the S&P 500 thanks to positive returns in Chinese stocks as Beijing ended its “zero-COVID” policy and commenced an economic reopening. Also, a falling dollar boosted global economic sentiment. Foreign developed markets outperformed emerging markets led, in part, by a bounce in United Kingdom stocks following the October resignation of PM Truss and the abandonment of her fiscal spending and tax cut plan. For the year, foreign developed markets registered negative returns, but after their fourth-quarter rally, outperformed the S&P 500.

For the month, the yield on 10-year Treasuries rose from 3.70% to 3.88%. As a result, intermediate investment grade bonds fell 0.5%. Most fixed income categories fell in December, but municipal bonds had a modest gain of 0.3%.

2022 in Review

Last year was the most difficult year for investors from a return and volatility standpoint since the Global Financial Crisis of 2008. Multi-decade highs in inflation combined with historically aggressive Fed rate hikes and growing concerns about economic and earnings recessions pressured both stocks and bonds. The S&P 500 posted its worst performance since 2008 while major benchmarks for both stocks and bonds declined together for the first time since the 1960s, punctuating just how disappointing the year was for investors.

The following points highlight the uniqueness of 2022 and why the year was so difficult to navigate for investors.

- Largest Inflation Increase Since 1981 –The most accommodative monetary policy in modern history which began following the Great Recession of 2008 and expanded through the COVID stimulus period led to a spike in prices not seen in generations. The U.S. CPI peaked at 9.1% in June. Inflation was a global problem impacting much of the developed world including the Eurozone, UK, Canada and Japan. In response, central banks reversed course and embarked on the most aggressive interest rate tightening cycle since 1980. Beginning in March, the Fed hiked rates rapidly by 4.25%. Both stock and bond markets were significantly impacted.

- Both Stocks and Bonds Declined by Over 10% – Last year was only the sixth time since 1926 that both the S&P 500 and Bloomberg U.S. Aggregate Bond Index declined. It is the only time in history where each fell by more than 10%. The U.S. stock market entered 2022 with the strongest bull market since the 1930s. By year-end the 2022 bear market became the longest since the 2007 to 2009 bear market, surpassing the bear market of 2015 to 2016. In the U.S. bond market, because of the unprecedented increase in interest rates, the Bloomberg index had its worst year on record.

- Steepest S&P 500 Earnings Slowdown Since 2011 – Entering 2022, corporate profits were growing at their fastest pace since 2010. Pent-up demand and pricing power led to strong revenue growth and record margins. Year-over-year comparisons grew tougher throughout 2022. Inflation and higher wages hurt profit margins. As a result, earnings growth decelerated at the steepest rate since 2011. With fourth quarter 2022 earnings season still to go; consensus estimates are calling for S&P 500 earnings per share to fall 8.5% in 2022.

- Geopolitics – China Lockdowns and Supply Chain Disruptions – While the rest of the world reopened, China continued with its zero-COVID policy through most of 2022. Entire cities were locked down for weeks if a few cases were found. Not only was the Chinese economy in shock from the closures, but trade to and from China was volatile. As expected, President Xi Jinping secured a historic re-election to a third term in October. After widespread protests over zero-COVID in November and December, the government lifted most restrictions. The MSCI China Index hit an 11-year low in October but rebounded into year-end.

- Geopolitics – Russia Invades Ukraine – The most critical event of the year, in terms of geopolitics, was Russia’s invasion of Ukraine on February 24. Russian President Vladimir Putin’s calculation that Europe would not rally to Ukraine’s side proved to be false. NATO galvanized to a degree not seen since the Cold War. Billions of dollars in weapons poured into Ukraine. Oil prices spiked and the U.S. materially depleted its strategic petroleum reserve. The impact was an almost certain recession for many European economies still struggling with the aftermath of COVID.

2023 Views and Commentary

The following are views impacting our recommendations in 2023:

- Inflation moderates but likely does not reach the Fed’s 2% inflation target rate by the end of the year

- Fed raises interest rates another 0.75% to a terminal level of about 5% and maintains tight monetary policy

- Recession expectations and corporate earnings more likely drive 2023 markets over Fed policy

- Elevated downside risk to S&P 500 earnings in 2023

- Equity / fixed income historical characteristics reassert diversification benefits, unlike 2022

- Lower valuations and a falling dollar could be tailwind for international stocks

- Housing sector challenged by high mortgage rates and inflation

- Geopolitical risks abound, both international and domestic

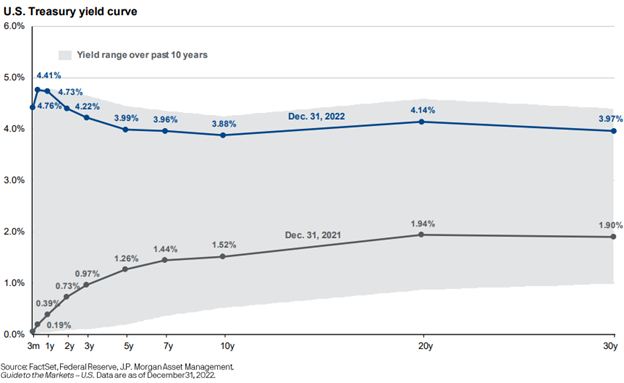

The U.S. economy is closer to a cycle peak. As the effects of inflation and higher interest rates take effect, recession is more likely in 2023. The Treasury yield curve, often seen as a warning sign for recession, recorded its steepest inversion in over 40 years as the 10-year Treasury yield dropped 78 basis points below the 2-year Treasury yield and remains inverted. Manufacturing activity, as measured by the Index of Industrial Production, recently posted a tepid gain, but is weakening. Housing data has been below expectations, and housing permits are at the lowest rate since the beginning of the pandemic. The consumer price index (CPI) fell from 9.0% in June to 7.1% in November. The near-term CPI readings will be critical for when the Fed can end interest rate increases. If the Fed must delay in its “pivot”, a recession could be deeper.

Corporate earnings drive long-term stock prices. In a recession when economic activity is contracting, how well the stock market holds up is directly related to the degree that earnings hold up. For now, consensus earnings expectations for the S&P 500 for 2023 are holding up. Estimates are modestly negative for the first half of the year, but then turn positive with full year 2023 estimated earnings growth of 4.8%. We are cautious regarding near-term earnings and earnings surprises. The next earnings reporting period will occur in the last half of January.

Fixed income yields are dramatically different from a year ago. The U.S. Treasury Yield Curve chart below shows the dramatic change from last year. Yields across all maturities are at or near ten-year highs. Bonds remain an important strategic piece of investment portfolios and the higher yields should mitigate negative effects from Fed rate increases in 2023. The era of zero / negative interest rate policies from central banks has largely come to an end.

As we start the new year, financial media commentary may be focused on the 2022 losses and current market risks, including earnings concerns and recession fears. But the market is forward-looking, and while there are undoubtedly economic and corporate challenges ahead in 2023, some of those best-known risks are partially priced into markets already, and there are likely potential positive catalysts lurking as we start a new year.

More broadly, market history is clear. Declines of the magnitude experienced in 2022 are usually followed by strong recoveries, not further weakness. The S&P 500 has not registered two consecutive negative years since 2002, while bonds, represented by the Bloomberg U.S. Aggregate Bond Index, have never experienced two negative consecutive years. That reality underscores an important point, that market declines such as 2022 have ultimately created substantial long-term opportunities in both stocks and bonds.

The stagflation of the 1970s and sky-high interest rates of the early 1980s eventually gave way to the strong economic growth and the market rally of the 1980s. The dot-com bubble burst of the early 2000s was followed by substantial market gains into the mid-2000s. The financial crisis of 2008, which perhaps remains the most dire economic situation experienced in modern market history, was followed by strong rallies in the years that followed.

As such, while we are prepared for continued volatility and are focused on managing both risks and return potential, we understand that a well-planned, long-term-focused, and diversified investment approach can withstand virtually any market surprise and related bout of volatility, including multi-decade highs in inflation, historic Fed rate hikes, geopolitical unrest, and rising recession risks.

At JMG, we understand the risks facing both the markets and the economy, and we are committed to helping our clients to effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint. Therefore, it’s critical to stay invested, remain patient, and stick to the established plan for each client’s personal asset allocation target based on their unique financial position, risk tolerance, and investment timeline.

That said, we continue to evaluate all asset classes for any tactical investment opportunities that may arise in this environment.

If you have any questions, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).